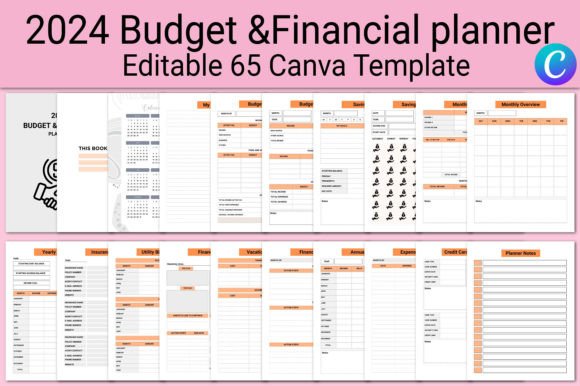

Master Your Money with the 2024 Budget Financial Planner

Money feels personal because it is. A single missed bill, an unexpected car repair, or a holiday season that stretched a little too far can unravel months of careful effort. The 2024 Budget Financial Planner offers something different from the usual spreadsheet or generic app—it gives you a physical, visual, and deeply customizable system designed to put every dollar in its place across the entire year. Spread across 65 different pages in a clean 8.5×11 inch format with no bleed, this planner turns abstract numbers into something you can see, touch, and actually follow through on.

What makes this particular planner stand out is how it mirrors real financial life. It does not ask you to squeeze everything into one or two categories. Instead, it acknowledges that money moves in many directions—bills, subscriptions, savings goals, debt repayment, sinking funds, travel dreams, and even the occasional online shopping splurge. By giving each of those a dedicated space, the 2024 Budget Financial Planner helps reduce the mental load of keeping track of everything in your head.

Why a Physical Planner Still Wins in a Digital World

Apps are convenient until notifications pile up and you start swiping past them without thinking. A physical planner sits on your desk or table, quietly present. Writing things down by hand has been shown to improve memory retention and commitment to goals. When you physically fill in a Monthly Budget page or color in a savings tracker, the act itself reinforces intention. The 2024 Budget Financial Planner takes advantage of this simple psychological truth—seeing your progress on paper feels more real than watching a number change on a screen.

There is also the matter of focus. A phone holds distractions; a planner holds only what you put into it. For anyone who has ever opened a banking app to check a balance and ended up scrolling social media, the benefit of a dedicated, distraction-free tool becomes immediately clear.

Breaking Down the Core Sections and Their Practical Value

The planner is organized around a full calendar year from January through December 2024. Each month includes a Monthly Overview page that lets you see income, expenses, and savings at a glance. This bird’s-eye view is helpful for spotting patterns—maybe you consistently overspend in the third week of the month or notice that certain months carry heavier utility costs. Recognizing these rhythms allows you to plan ahead rather than constantly reacting.

Beyond the monthly spreads, the planner includes a Yearly Overview and Yearly Income tracker. These pages are especially useful for freelancers, gig workers, and small business owners whose income fluctuates. Tracking annual earnings in one place simplifies tax preparation and helps you understand your true earning capacity over time. Pair that with the Tax Deduction tracker, and you have a practical system for capturing deductible expenses throughout the year instead of scrambling in April.

Expense Tracking That Goes Beyond the Basics

Most people underestimate what they spend by a significant margin. The Expense Tracker and Spending Tracker pages encourage honest recording. What makes this system more thorough is the inclusion of specialized trackers for areas that often slip through the cracks: Online Shopping Tracker, Bills Subscriptions log, and a Credit Card Information page. Subscription creep is a quiet budget killer—streaming services, apps, and membership boxes add up quickly. Having a dedicated space to list them all, along with billing dates and amounts, makes it easier to spot what you truly use and what you can cut.

The Quarterly Bills Tracker and Utility Bills Tracker serve a similar purpose for recurring household expenses. Quarterly payments like water, trash, or HOA fees can catch you off guard if you are only thinking month to month. Tracking them separately builds awareness and prevents those surprise moments when a bill arrives and disrupts your regular cash flow.

Savings Goals That Feel Achievable Rather Than Abstract

Saving money without a specific target often fizzles out. The 2024 Budget Financial Planner addresses this by including multiple goal-oriented savings trackers. One of the most engaging features is the set of structured challenges: the 10 Savings Challenge to save $1,000, the 15 Savings Challenge for $1,500, and the more ambitious 100 Savings Challenge aimed at $10,000. Each breaks a large number into smaller, manageable increments. Instead of thinking “I need to save ten thousand dollars,” you focus on completing the next box in the tracker. That subtle shift makes the goal feel reachable.

For those focused on security, the 3-6 Month Emergency Fund Savings Tracker provides a clear visual path toward building a financial safety net. In a year where economic uncertainty remains a concern, having a dedicated tracker for emergency savings is less about optimism and more about practical preparedness. The Month Ahead Savings page also helps you work toward the goal of living on last month’s income—a strategy that reduces stress and breaks the paycheck-to-paycheck cycle.

Life Stage Funds and Personal Dreams

People save for wildly different reasons, and the planner respects that. The Wedding Fund, Baby Fund, Travel Fund, and Dream Fund pages give a home to goals that might otherwise feel frivolous compared to practical expenses. Giving these dreams a dedicated page legitimizes them—it says that wanting to travel or plan a wedding is a valid financial priority worth tracking alongside bills and debt payments. The Vision Board page adds a creative, aspirational layer where you can attach images or write descriptions of what you are working toward, connecting the numbers to something emotionally meaningful.

The Vacation Budget page deserves special mention. Planning a trip often involves estimating costs and then watching those estimates balloon. Breaking down transportation, lodging, food, activities, and souvenirs into a single, organized page helps you set realistic expectations and avoid post-vacation credit card regret.

Debt Management Tools With a Focus on Progress

Debt repayment can feel like running uphill in sand. The Debt Snowball Tracker applies the popular method of listing debts from smallest to largest, then focusing extra payments on the smallest balance while maintaining minimums on others. Watching debts get crossed off one by one builds momentum. This visual chain of small wins is often what keeps people committed to a repayment plan when the total amount feels overwhelming.

Alongside the snowball tracker, the Bank Account and Checkbook Register pages maintain a clear record of account balances and transactions. For anyone who shares finances with a partner or manages multiple accounts, these pages reduce confusion and help catch errors or unauthorized charges quickly.

Retirement, Net Worth, and Long-Term Thinking

Short-term budgeting matters, but long-term awareness changes behavior. The Retirement Tracker and Retirement Savings pages provide a place to record contributions, investment balances, and progress toward your retirement number. While this planner is not a full investment management tool, having retirement visibly represented alongside monthly expenses reinforces the importance of paying your future self consistently.

The Net Worth page is one of the most revealing tools in the entire planner. Listing all assets and liabilities in one place gives you an honest snapshot of financial health. Tracking net worth quarterly or annually reveals trends that monthly budgeting alone might miss. For many, this page becomes a grounding exercise—a reminder that financial progress is measured not just by income but by the gap between what you own and what you owe.

Sinking Funds, No Spend Challenges, and Behavioral Shifts

The concept of Sinking Funds—setting aside small amounts regularly for predictable but irregular expenses—is woven throughout the planner. Instead of being caught off guard by car maintenance, holiday gifts, or annual insurance premiums, you fund these categories bit by bit. The sinking funds pages let you assign a purpose to your savings so that when the expense arrives, the money is already waiting.

The No Spend Challenge tracker introduces a behavioral experiment that many find eye-opening. Committing to a day, week, or month of zero discretionary spending forces you to distinguish between wants and needs in real time. Recording your no-spend streaks in the planner adds accountability and can reset spending habits that have drifted toward mindless consumption.

Practical Considerations and Who Will Benefit Most

This planner works best for people who enjoy a hands-on approach to money management. If you appreciate structure but also want flexibility, the variety of 65 pages means you can focus on the sections most relevant to your situation and skip or lightly use the rest. The Canva link included with purchase allows digital editing before printing, which is helpful for those who prefer typed entries or want to customize certain layouts. Files come in JPG, PNG, and PDF formats, giving you options for printing at home, at a print shop, or using the pages digitally on a tablet with a stylus.

Freelancers and small business owners will find the income tracking, tax deduction, and expense pages particularly useful for separating business and personal finances. Educators and bloggers who manage multiple income streams can use the Paycheck Budget and Annual Finance pages to smooth out irregular earnings. Creators saving for equipment upgrades or big projects may gravitate toward the goal-specific funds. Parents managing a household budget will appreciate the bill trackers and sinking funds for predictable kid-related expenses like sports fees, school supplies, and birthday parties.

That said, this planner may not be the best fit for everyone. Those who strongly prefer automated budgeting through apps like YNAB or Monarch may find manual tracking redundant. If you rarely have time to sit down and write, a physical planner could end up unused on a shelf. The key is honest self-assessment—do you engage more deeply with paper tools, or do you need the nudges and integrations that software provides? Some users actually combine both approaches, using an app for daily transaction tracking and the planner for weekly reviews and goal setting.

The Planner Notes, My Notes, and general Notes pages offer open space for reflections, adjustments, or recording financial lessons learned throughout the year. These unstructured pages often become the most personal part of the planner—a place to jot down salary negotiation outcomes, ideas for side income, or reminders about why a particular savings goal matters in the first place.

For anyone looking to take control of their finances in 2024 without relying entirely on screens, the 2024 Budget Financial Planner provides a comprehensive, thoughtfully organized system. It does not promise overnight wealth or magical solutions. What it offers is clarity, structure, and the satisfaction of watching your financial picture improve one tracked dollar at a time.